. Lately, the non-performing loan ratio of banks and financial institutions has been on the rise. As a result, banks and financial institutions have been increasing the amount set aside for loan loss provision.

As of the second month of the current fiscal year, Rs TAG_OPEN_div_86 284.71 billion has been allocated for risk management of banks and financial institutions. The amount allocated for risk management of banks and financial institutions has increased by 24.64 percent compared to the same period of the last FY. In the last fiscal year, such amount was Rs 228.42 billion.

In the first two months of the current fiscal year (up to mid-September), commercial banks have allocated Rs 245 TAG_OPEN_div_84.83 billion for loan loss provision. Similarly, development bank has allocated Rs 27.93 billion while finance companies have allocated Rs 10.93 billion.

The amount allocated by banks and financial institutions for loan loss provision has increased significantly in the same period of the current fiscal year compared to the two months of the last fiscal year.TAG_OPEN_div_82 The loan loss provision of commercial banks has increased by 23.16 percent compared to the previous fiscal year. Similarly, the growth rate of development banks and finance companies by 43.41 percent has increased.

The loan loss provision has increased significantly due to the increase in non-performing loans (NPLs) of banks and financial institutions.TAG_OPEN_div_80 As the risky loans of banks and financial institutions increase, the provision amount should be increased. Due to the loan loss provision, the profit of the banks has not improved significantly. This will also have an impact on the dividend that the bank pays to the shareholders in the long run.

There has been no demand for loans in the bank for a long time. The loan has not been disbursed on time. Banks are under pressure to raise loans. The private sector, which takes loans, is getting more and more frustrated for various reasons. The country’s unstable politics, the Genji agitation of September 23/24 and the damage it has caused and the fear it has created in the private sector have made industrialists and businessmen worried about how to secure their investment rather than taking loans.

After the recent political incident, private sector organizations like the Federation of Nepalese Chambers of Commerce and Industry (FNCCI), Confederation of Nepalese Industries (CNI), Nepal Chamber of Commerce and Industry have been demanding guarantee of security in the industry.TAG_OPEN_div_76 They have been demanding the government time and again to create an environment for industries to do business.

When there is no credit flow or business in the private sector, it affects not only the private sector but also the banking system. There will be no loan flow. The loan given will not be repaid. And banks should increase the amount of money they have earmarked for potential credit risk.

Bad loans are increasing in banks due to the inability to recover the interest on the loan on time. As a result, bankers say that a large amount of money has to be set aside for loan loss provision.

As of mid-September of the current fiscal year, the average NPL of the banks and financial sector has reached 4.62 percent.TAG_OPEN_div_70 During this period, the NPL of commercial banks increased by 4.44 percent, development banks by 5.03 percent and finance companies by 11.05 percent.

The bank’s non-performing loans have been increasing for some time due to financial problems in the construction, industry and real estate sectors.TAG_OPEN_div_68 The Nepal Electricity Authority (NEA) on October 19 and 20 disconnected the power supply to 25 different industries, citing non-payment of dues of Rs 6 billion for dedicated feeders and trunk lines. What will be its impact will be seen in the future.

The Nepal Rastra Bank (NRB) has made a provision to classify the loans issued by banks and financial institutions and keep the loan losses accordingly.TAG_OPEN_div_66 Banks should now make provision of 1.25 per cent for good loans, 5 per cent for micro-surveillance, 25 per cent for substantive loans, 50 per cent for doubtful loans and 100 per cent for bad loans. According to this provision, the banks have made provisions.

As soon as the bank disburses a loan, it should be classified as a good loan and make a provision of 1.25 percent.TAG_OPEN_div_64 A provision of 5 percent should be made by keeping the principal under close supervision for 3 months after issuing the loan. If the principal interest is not paid for 3 to 6 months, then a provision of 25 percent should be made by classifying it as a subordinate loan.

Similarly, if the principal interest is not paid for 6 months to 12 months, then a 50 percent provision should be made by classifying it as a doubtful loan.TAG_OPEN_div_62 In the loan that has not been paid for more than one year, the bank goes to the loan recovery process by making a hundred percent provision.

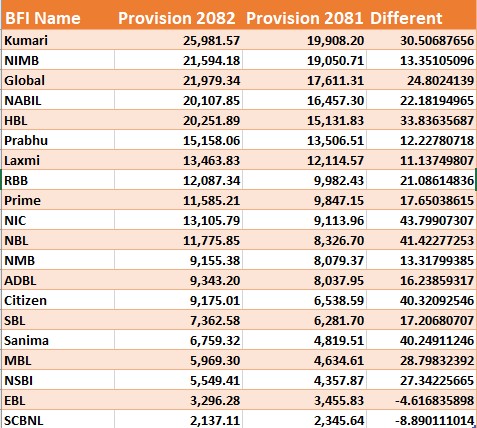

Kumari Bank has the highest loan loss provision in commercial banks, how much is it of other banks?TAG_OPEN_strong_47

Kumari Bank has set aside the highest amount of loan loss provision for the second month of the current financial year.TAG_OPEN_div_59 As of mid-September, Kumari Bank has a loan loss provision of Rs 25.98 billion. According to Nepal Rastra Bank, the provision of Yes Bank has increased by 30 percent in one year. In the last fiscal year, the bank had a provision of Rs 19.90 billion.

Similarly, Akro Bank Nepal Investment Mega Bank has the highest number of provisions.TAG_OPEN_div_57 The bank has a net worth of Rs 21.59 billion as of the second quarter of the current fiscal year. Global IME Bank, Nabil Bank and Himalayan Bank have a provision of more than Rs 20 billion. Prabhu Bank has a provision of over Rs 15 billion while Laxmi Sun Raj Bank has a provision of Rs 13 billion.

Stats

}

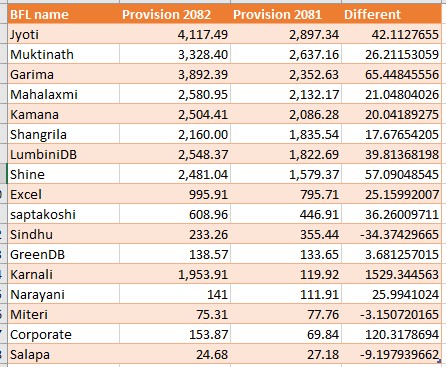

Development Bank has the highest provision of Jyoti Bikas, how many others?

Jyoti Bikas Bank is the largest development bank with the highest provision till the second end of the current fiscal year.TAG_OPEN_div_52 The bank has made a provision of Rs 4.11 billion in the second quarter of the current FY. The bank’s provisions have increased by more than 42 percent compared to the last fiscal year. Similarly, Muktinath Bikas Bank has allocated Rs 3.89 billion for the provision. This has increased by 26 percent compared to the last fiscal year.

प्रतिक्रिया दिनुहोस्